When higher for longer’ interest rates start disrupting life for the masses!

Markets finally get the message…Cynics argue that marking the end of the hiking cycle is easy:

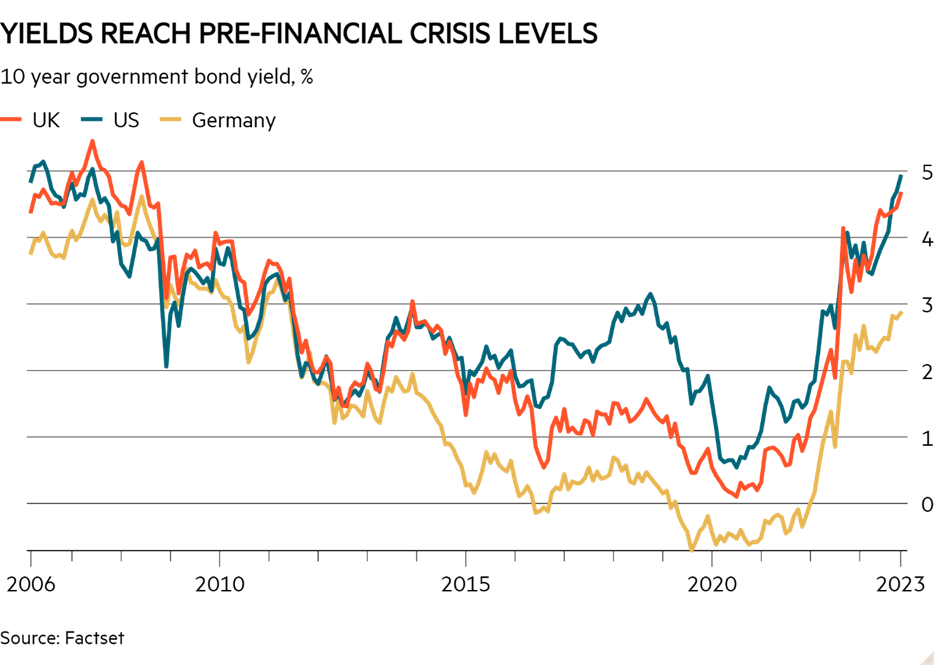

Central bankers just raise rates until something in the financial system breaks. Earlier this month, things certainly looked precarious – as the chart shows, government bonds sold off and pushed 10-year yields to pre-financial crisis highs. The US 10-year Treasury yield even surpassed the important 5 per cent mark. Following the spike, Steen Jakobsen, chief investment officer at Saxo, said “we have clearly reached a stage where something is breaking the real rates are too high and the global economy is about to tilt down while central bankers are asleep at the wheel.”

What triggered the sell-off?

Monetary policy looks like a key culprit, although speculators are another.

Pimco (US investment house) economists suggested that ongoing economic resilience has reduced the chance of recession. Because of this, markets expect quantitative tightening programmes to march onward, which means high levels of government bond supply. Pimco believes investors are demanding a higher premium for holding longer maturity bonds as a result.

Uncertainty about the outlook for inflation and monetary policy received less coverage but also looked like a convincing trigger. According to analysts at Capital Economics, the ‘higher for longer’ message pushed by Fed officials last month lines up nicely with what they call the “latest bloodbath in bonds.”

Is this good news for central banks?

On one hand, yes: all the Fed dot plots and Table Mountain comparisons have done their job, and markets have come around to the idea of higher for longer rates. Higher bond yields should contribute to tighter financial conditions, complementing the interest rate hikes implemented so far and helping in the fight against inflation. But will tightening go too far?

Earlier this month, Berenberg economists stressed that the government bond market occupies a unique position as the risk-free benchmark. As such, it “acts as the conductor of the grand financial market orchestra. To every move in sovereign yields, equities, credit, and currencies all respond in concert.” This means that increases in longer-dated bond yields tend to be transmitted to the economy more aggressively than changes to the policy rate set by central banks.

Thanks to very long-time lags, only around half of the impact of central bank tightening has been felt in the economy so far. Analysts estimate that (in the eurozone, at least) an increase in longer-term interest rates has a four times stronger impact on growth than a policy rate hike of the same size.

Carsten Brzeski, global head of macro at Dutch bank ING, calculates that the 50-basis point surge in bond yields could have already had the same impact on economic activity as half of the policy rate hikes seen in this tightening cycle so far. According to Capital Economics’ Financial Conditions Index, conditions have already tightened enough to exert a significant impact on interest rate-sensitive areas of the economy over the past few weeks.

Can rates really stay higher for longer?

As it stands, the risk of ‘overtightening’ looks very real due to the combination of policy rate hikes feeding through and the rise in longer-term interest rates. Economists fear that this could push the US, UK, and European economies into recession – or cause something in financial markets to break.

This all means that it is unclear whether rates really will stay high for as long as markets currently expect. Analysts at Capital said that “the sheer sale of the bond market sell-off is about to face a reckoning with reality” and think that lower inflation and weaker growth will make it hard for central banks to keep interest rates high past the middle of 2024. And this creates an unpalatable dilemma for central bankers, “the irony of such a scenario would be that the more financial markets believe in ‘higher for longer,’ the higher the chances are that central banks will actually cut rates”.