The artificial intelligence boom is boosting demand for data centres across the world. Howe can private investors profit from it? Val Cipriani reports

Written by Val Cipriani – February 22, 2024

The email you sent to your most important client last week. The WhatsApp message inviting your daughter for dinner on your birthday. The picture of your dog covered in mud at the end of the Sunday walk. There’s a place that sees, houses and makes possible every little thing you do online, from the music you listen to, to doing your grocery shopping.

From the outside, it looks like just another giant warehouse. But inside are not aisles of boxes but thousands of computers, which means it uses up vast amounts of electricity and water and is protected by sophisticated security systems. The place is a data centre. Or, more accurately, many different data centres, depending on the digital services you use.

These centres host the physical infrastructure necessary to run digital applications and services, as well as manage and store the data that goes with them. As we produce and consume more data, we need more data centres.

And we have been producing and consuming a lot more data. Remember floppy disks? A standard one had a memory of 1.44 megabytes. Now a single photo on your phone can take up 6 megabytes or more. According to intelligence firm IDC, in 2017 the amount of digital data created worldwide was approximately 32 zettabytes (one zettabyte is equivalent to a trillion gigabytes). This is forecast to reach 291 zettabytes by 2027 – a ninefold growth rate, meaning a compound annual growth rate of 25 per cent.

In 2022, Savills estimated that Europe’s pipeline of data centres would need to more than double by 2025 to meet demand for storage. Demand in key European cities was up by 20 per cent year on year as of the third quarter of 2023, according to research by real estate adviser JLL.

DATA CENTRES CONSUMED SOME 18 PER CENT OF IRELAND’S ELECTRICITY IN 2022.

There is much more on the way. Growth in data creation has been a trend for years, but artificial intelligence (AI) promises to accelerate it. A Schroders report says that it is “clear” that Nvidia’s (US:NVDA) advanced graphics processing units (GPUs), which have the capability to process the large amounts of data needed for training and applying AI models, “entirely depend upon high-performance, secure, and stable data centre environments”.

For investors, data centres can be a different ‘picks and shovels’ way to play the AI trend, less racy than investing in chipmakers. But gaining exposure from the UK is not straightforward, as the highest-profile investment trust tapping the trend is now making an ignoble retreat, and the industry itself has challenges to contend with, from power generation to high interest rates.

Supply vs demand

As an investment, data centres sit somewhere between infrastructure and real estate. In broad terms, they make money by renting out space, equipment and services to internet companies. They have leases that can last seven years or more, with annual rent increases built in, meaning they generate a regular, rising income.

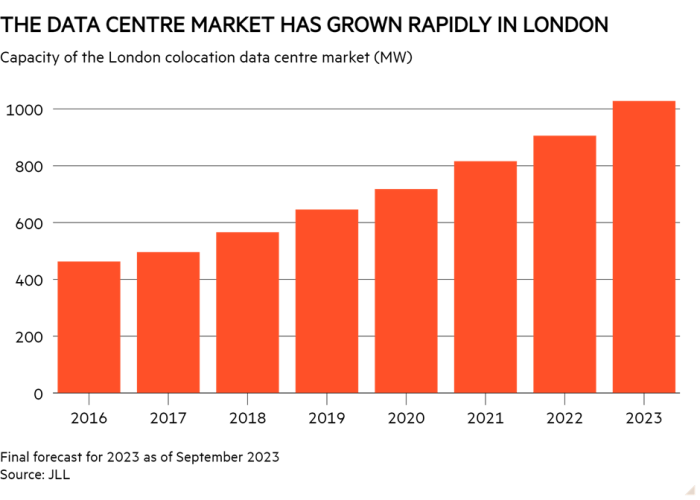

The supply of these buildings has risen rapidly in recent years in a bid to keep up with demand. In London alone, data centre capacity more than doubled from 496MW in 2017 to an estimated 1,028MW at the end of 2023. But while the pipeline is still sizeable, JLL notes that recent months have seen “a combination of schemes getting pushed further back and difficulty acquiring both land and power”.

Tom Walker, co-head of global listed real assets at Schroders, likes the asset class compared with other areas of real estate because of supply constraints like these. He contrasts the situation to the ecommerce trend that boosted demand for logistics hubs while shipping centres struggled, starting about a decade ago. “We all went overweight logistics assets and underweight retail. But what happens when a sector starts to make supernormal returns is that you get a supply response. So more logistics get built and, as strong as the underlying trend is, the rental increase that we saw four or five years ago [in the logistics sector] is now slowing,” he says.

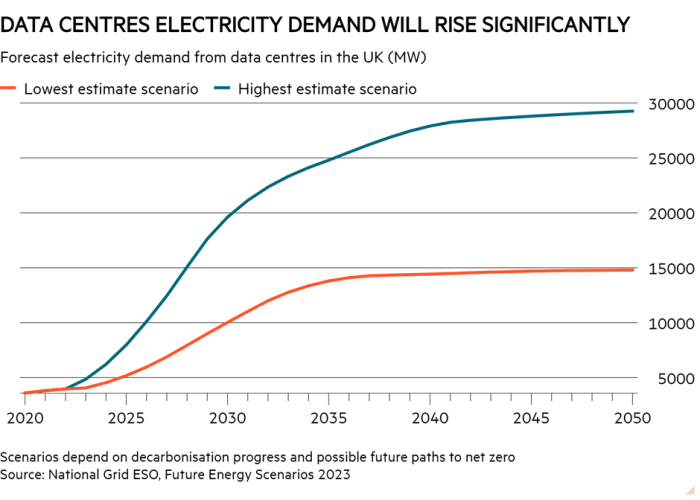

The same pattern may not play out for data centres, because building a warehouse and getting a data centre online are not the same thing. The latter needs land with access to fibre connection and a lot of power. The International Energy Agency estimates that global electricity demand from data centres could amount to double 2022 levels as soon as 2026. As a result, governments have become more reluctant to grant permission for the construction of new centres.

Data centres consumed around 18 per cent of Ireland’s electricity in 2022, and this could reach 30 per cent by 2030. In response, state grid authority EirGrid has stopped supplying new connections in Dublin until at least 2028, resulting in project delays and cancellations. Other countries such as Germany, Singapore and China have also introduced restrictions. Meanwhile, National Grid ESO, part of National Grid (NG.) estimates that commercial data centres could make up 6 per cent of the UK’s electricity demand by 2030, up from 1 per cent in 2023.

In Europe, JLL analysts describe “a supply-demand imbalance” for co-location data centres (those that cater to multiple small and mid-sized businesses). Prices have gone up as a result, with an estimated 15 per cent increase to co-location rents in 2023 that the analysts expect will continue in 2024.

The combination of high demand and constrained supply, driven by a strong underlying trend, means that data centres sit at the more growth-focused end of the spectrum of real estate and infrastructure, together with other types of digital infrastructure such as fibre and towers.

Because of the fundamental need for new data centres, there is a big opportunity for companies to deploy capital into new facilities, says Fred Heaton, research analyst at Investec Wealth & Investment. But on top of regulatory issues and energy requirements, developers have to contend with the increased cost of capital in a high-rate environment, which means achieving that growth is not a done deal. So investors need to weigh rental growth prospects against the possibility that new projects suffer setbacks – a scenario that has caused problems for other infrastructure sectors over the past couple of years. Heaton is still confident, however: “Once you factor in both organic and inorganic growth, assuming companies can tap the market for new equity and have continued access to debt capital to fund their development pipelines, then a low double-digit top-line growth rate is not wildly optimistic.”

Challenges

If AI looks like a big opportunity, it will also bring some challenges. Generative AI requires more performance-intensive infrastructure than is found in standard data centres, producing much more heat. Nvidia has turned to an innovative liquid cooling system for its processors, because the air cooling used as standard is not enough. Operators will need to adapt their facilities accordingly.

There is also a question of whether independent operators will actually be able to profit from the AI revolution. The big tech companies have the capital and capacity to build and operate their own facilities. At the beginning of the year, Google announced a $1bn (£790mn) investment in a new centre in Hertfordshire.

But supply constraints also apply to the tech giants, particularly when they need to have a presence near the biggest cities to minimise latency. Walker explains: “You can’t just come into London, Tokyo or Sydney, buy a piece of land and build a data centre, even if you’ve got all of Amazon’s money. If they want to have data centres in all these key global cities, they are going to have to deal with third parties.”

US data centre operator Equinix (US:EQIX) recently announced a partnership with Nvidia to offer the chip company’s supercomputing systems to corporate clients, which suggests that operators can find opportunities in the AI ecosystem. Heaton adds that, at some point, tech giants might want to sell in-house facilities to specialists such as Equinix and lease them back, in order to get them off their balance sheets – a trend previously seen in the supermarket sector, to name one example.

Accessing clean energy is also a major issue. The industry is pivoting towards renewables, but Hiral Patel, global head of sustainable and thematic research at Barclays, notes that in most countries the majority of data centres connect to their local electricity grid, where non-renewables still make up a significant part of the electricity mix. Meanwhile, since uninterrupted power supply is crucial, they typically deploy diesel or gas back-up power in the event of a blackout.

One of the reasons Ireland is struggling to keep up with electricity demand is that its grid is ageing, and it’s far from alone in this regard. “Electricity grids around the world will not be able to cope with increased AI workloads. This will increasingly put data centre operators in a precarious position,” Patel says. Data centres also use up large amounts of water for their cooling systems, to the point that in July 2023, Thames Water indicated that it was considering measures to curb their water usage, including charging more at peak times and out-and-out restrictions.

How to invest

The most direct way of getting exposure to data centres is via a listed owner and operator. The largest are US-listed Reits Equinix and Digital Realty (US:DLR). Like most Reits, both initially proved sensitive to interest rate hikes in 2022, before shares rebounded significantly last year as investor appetite for all things AI took over.

Digital Realty currently looks slightly cheaper at a forecast price/funds from operations (FFO) ratio of 20.7 times, against 23.9 for Equinix. As of January 2024, both were among the 10 Reits trading at the largest premiums to net asset value (NAV) estimates in the US, with an estimated premium of 17.9 per cent for Equinix and of 13.8 per cent for Digital Realty, according to S&P Global Market Intelligence data. Such premiums will appear particularly expensive in the eyes of UK Reit investors. But US Reits follow different accounting rules, do not have to periodically update their NAVs (hence why premiums are estimated) and instead are usually evaluated according to their cash flows.

Walker notes that the two companies partly operate in different areas of the market, with Equinix focusing more on colocation data centres and Digital Realty on the so-called hyperscalers: big cloud computing companies such as Microsoft and Amazon. “With the advent of artificial intelligence and the dramatic increase we’re seeing in the demand for data centres from these hyperscalers, we think Digital Realty is probably likely to see stronger rental growth at this point in time,” he argues.

AT THE BEGINNING OF THE YEAR, GOOGLE ANNOUNCED A $1BN INVESTMENT IN A NEW CENTRE IN HERTFORDSHIRE

But that is not the only factor at play. Barclays analysts are underweight Digital Realty and neutral on Equinix. “Equinix continues to offer the most widespread low-latency connectivity of any of its competitors, and we think the company is well positioned to participate in future AI demand,” they say. “But its facilities are priced at a premium and companies have become more conservative on spending.” The company released a solid set of annual results for 2023, with revenue up 13 per cent year on year, adjusted Ebitda 10 per cent higher and a 45 per cent adjusted earnings margin.

Meanwhile, Digital Realty had to recapitalise its balance sheet last year through asset sales and equity issuance, which the analysts think may limit earnings growth in future. They like the prospects of a third US Reit, Iron Mountain (US:IRM), which offers data centres but also a range of other services to businesses, including records management. Another listed data centre operator is the Australian NextDC (AU:NXT).

UK Reits do not offer much exposure to the trend. The partial exception is warehouse landlord Segro (SGRO), which leases some of its warehouses to data centre operators. Its Slough trading estate, which accounted for 16 per cent of the portfolio as of the end of 2022, has the second-largest hub of data centres in the world, the company says.

Heaton says that while “it would be great” for a Reit specialising in the area to list in London, it would likely need a more favourable funding environment. The US Reit market is more mature and less demanding from a regulatory perspective, he argues.

In the UK, investors can gain exposure via infrastructure trusts, but the catastrophic performance of the main trust in this area provides a classic example of the fact that an exciting trend does not always translate into good, or even acceptable, investment returns.

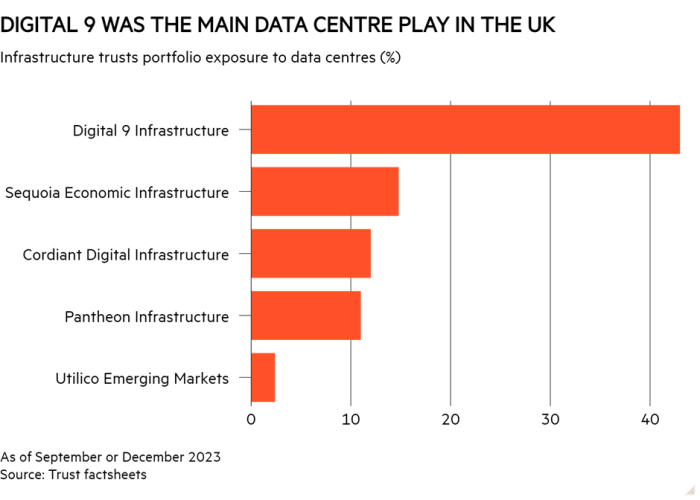

Digital 9 Infrastructure (DGI9) had 43 per cent of its portfolio in data centres as of September 2023. But the trust has started what promises to be a complicated wind down process following a series of issues with its debt and balance sheet. Ben Mackie, fund manager at Hawksmoor Investment Management, notes that while Digital 9’s data centre business was actually growing quickly, the need for follow-on investment meant the trust overstretched its cash position in order to provide funding, as well as to make other deals and pay its dividend.

Cordiant Digital Infrastructure (CORD) is the other trust dedicated to digital infrastructure, but has a much lower exposure to data centres, and the rest of the portfolio is split between communication towers and fibre. This is primarily via Hudson Interxchange, an interconnect data centre and platform provider located at 60 Hudson Street in New York. Originally the headquarters for Western Union, the building has long been a key crossroad for communications in Manhattan, and Digital Realty also operates there. Cordiant says that interconnect data centres are like ‘digital crossroads’ and because of their position and the essential service they provide they can charge a premium to traditional colocation services’ rates.

Mackie cautions that like Digital 9, Cordiant is not a vanilla infrastructure trust, generating safe cash flows with limited growth prospects. Instead, it offers higher growth potential but is closer to a private equity type of investment. Its portfolio is concentrated and the trust relies on the same ‘buy and build’ strategy as Digital 9, which entails using fresh equity or cash flows to make acquisitions and increase capacity. But Cordiant has set a more conservative dividend target, avoided stressing its balance sheet and can still execute its strategy despite the tougher macroeconomic environment, Mackie says.

As of 13 February, Cordiant was trading at a discount to NAV of 43.7 per cent, the second highest in the AIC infrastructure sector after Digital 9 itself. This will partly be because investors are wary of the sector after Digital 9’s tribulations, but infrastructure trusts have also had to contend with a wider set of challenges in the past two years, from high interest rates impacting valuations to competition from fixed income.

The other options to gain exposure to data centres are Pantheon Infrastructure (PINT) and Sequoia Economic Infrastructure Income (SEQI). The first runs a diversified range of infrastructure assets, with 44 per cent of the portfolio in digital infrastructure and the rest split between utilities, renewables and transport. Sequoia also invests across different infrastructure sectors but is a debt trust, with a pretty attractive yield of 8.1 per cent. Utilico Emerging Markets (UEM), which focuses on listed infrastructure businesses in emerging markets, also has a small allocation via Korean Internet Neutral Exchange, a Korean data centre operator.

There are also less direct ways to access the trend. The IC’s small-cap expert Simon Thompson notes that building services contractor TClarke (CTO) is well-positioned to profit from the growth of data centre demand. Barclay’s Patel flags Greencoat Renewables (GRP) and Gore Street Energy Storage (GSF) as two renewable energy trusts that offer investor exposure to the theme of “green data centres”. This is partly because they both have significant exposure to Ireland, where renewable energy generation and battery storage will be crucial to meet data centre electricity demand.

In the years ahead, operators will need to adapt to a tougher regulatory and funding environment and scale up their sustainability efforts. But with AI still in its infancy and global data creation set to grow fast, demand for data centres is not going anywhere – quite the opposite. Despite the challenges, the strength of this trend coupled with supply constraints should give companies in the space resilience, pricing power and a growth potential that can still offer something to investors.